How climate and environmental risks become financial problems

We are all effected by the impacts of climate change, and are becoming more aware of the consequences. It has proven to be difficult to estimate the potential consequences, and it doesn’t help that the terminology and concepts continue to change.

Climate-related and environmental (C&E) impact analysis is becoming the widely used approach to anticipate and mitigate the impacts from C&E events; however, recently our assignments have shown some of the new terminology and concepts can be obstacles for members of the project. Moreover, the gaps within guidance and best practice reports for financial institutions require abstract approaches when starting to assess the traditional risks and impacts from C&E events. Therefore, we wanted to clarify the main concepts and pathways whereby traditional financial risks might occur from C&E events.

Climate-related & environmental risks

Financial institutions experience complex risk exposure from C&E events that develop through various channels. A climate or environmental event can become a risk driver when it leads to risks and impacts on the economy and banks1. The C&E risk driver is either a physical risk or transition risk. Physical risks are extreme weather events, such as floods, or long-term gradual shifts in the climate, such as sea level rises or higher average temperatures1. Alternatively, a transition risk occurs from human effort to address C&E challenges, such as new policy implementations, new technological developments or changes in public sentiment.

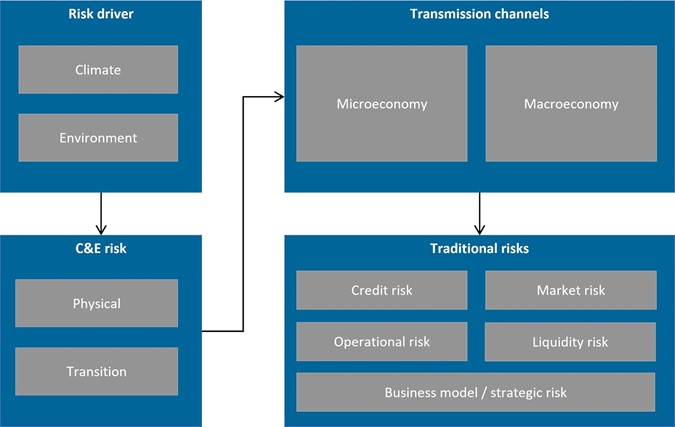

Figure 1: C&E risk driver relationship to traditional risks

Figure 1: C&E risk driver relationship to traditional risks

Given the current global climate circumstances, C&E events and risks are increasing both in frequency and severity, prompting investigation into C&E risk drivers and how they transmit to traditional financial risks. These ‘transmission channels’ are characterized at high-level macroeconomic perspective, such as higher borrowing costs or limited financial markets, or a granular-level of the microeconomy, such as individual elements or direct effect on financial institutions, for example assets and household values decreasing1.

Research has shown as climate-related events occur, corresponding reactions in the economy follow, leading to impacts on traditional financial risks (refer to Figure 1). Various methodologies are available to understand C&E risk impact; however, since research is ongoing, there is no standard method to assess the impacts.

Transmission channels

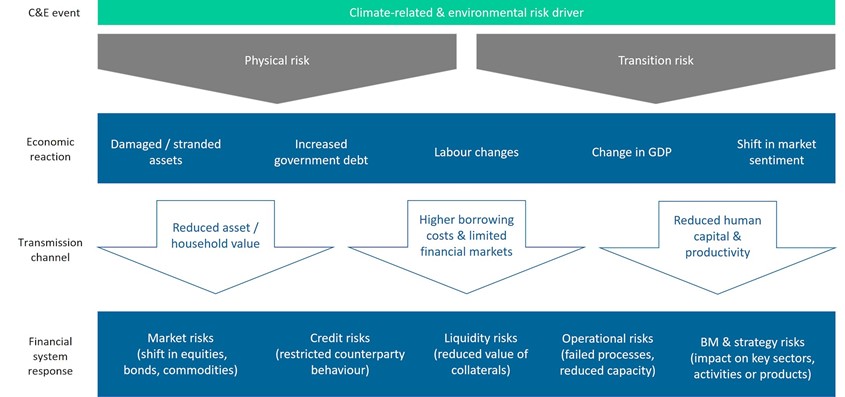

Given the novelty of C&E risk analysis and considering C&E events occur in non-linear and uncertain ways, identification of the risks and opportunities remain highly abstract. The visual below shows an example of how a C&E risk driver – through transmission channels – can develop into traditional risks. It’s important to note that C&E risk drivers and transmission channels can act interdependently when considering a future scenario. For example, the rise in GHG (Greenhouse Gas) emissions leads to multiple transition and physical risks, ultimately leading to numerous impacts on a financial institution.

Figure 2: Possible C&E pathways to traditional risks

A significant limitation of current assessments is lack of adequate data and resources, restricting the ability and capacity to properly understand and estimate the outcome1&2. This causes weak mitigation practices due to unavailable or insufficient data and knowledge. Specifically, when identifying transmission channels, it’s difficult to narrow down and determine the most relevant causal chain between traditional risks and C&E risk drivers. The possible transmission channels vary and depend on hypothetical estimations, with existing literature focusing mainly on credit risk and marginally on market risk1. New data is needed to translate C&E risk drivers into economic risk factors, then into exposures and financial risk2.

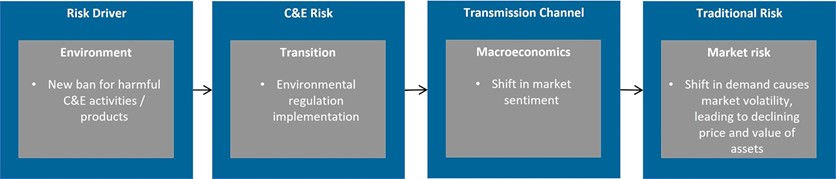

Figure 3: Environmental risk driver into market risk pathway

The example represented in Figure 3 shows one pathway whereby an environmental risk develops into a traditional risk, in this case increasing market risk. Further discussion on the consequences from a new ban on activities or products leads to much wider impact on a financial institution. If the assets that have been devalued are held for collateral, the credit risk increases due to the increased loss given default. Also making it more difficult to sell the devalued assets, increasing liquidity risk. Furthermore, the reputation of the financial institution is also directly linked to market sentiment, and when this shifts, the clientele and workforce will have new expectations that must be met in order to keep the stakeholders satisfied.

This example demonstrates that when a C&E event occurs, it will never be limited to one impact.

Lessons learned

The main outcomes from project experience and best practices indicate approaching C&E analyses across multiple time horizons, while accounting for a range of possible risks, utilizing current (internal and external) data and allowing enough time to analyse at a granular level. Institutions must individually approach C&E risk analysis to account for their specific. Additionally, using both qualitative and quantitative approaches will be the most comprehensive and therefore yield the most relevant outcomes. Otherwise, the lack of metrics can inhibit future action due to uncertain losses. However, in order to quantify initial findings, financial institutions must go beyond traditional risk management practices2.

The descriptive data from the transition and physical risks can be used to understand the influence on economic relationships, and the identification of priorities and vulnerabilities2. This information will then be the relevant transmission channels, and can lead to estimations of potential impacts on exposures.

Curious about these or other experiences, please contact us at info@4esgconsulting.nl

Sources

[1] Basel Committee on Banking Supervision (April, 2021). Climate-related risk drivers and their transmission channels.

[2] Basel Committee on Banking Supervision (April, 2021). Climate-related financial risks – measurements and methodologies.

Website door: